Toggle intro on/off

Woolworths (WOW) - 3Q26 sales result analysis

Sympathetic tone to shoppers

04 May 2026

Australian supermarkets - 3Q26 food & liquor sales preview

Look forward, not backwards

28 April 2026

Coles Group (COL) - FY24 result analysis

More ups than downs

30 August 2024

Woolworths (WOW) January 2024 trading update

Difficult outside the core

31 January 2024

Australian supermarkets - grocery perspectives

Prices, profits and government scrutiny

31 January 2024

Woolworths (WOW) 3Q23 result insights

Inflation support is softening

04 May 2023

Metcash (MTS) 1H23 result insights

The benefits of inflation

05 December 2022

Woolworths 1Q23 result insights

It gets better from here

05 November 2022

Coles 1Q23 result insights

A low point in sales growth

28 October 2022

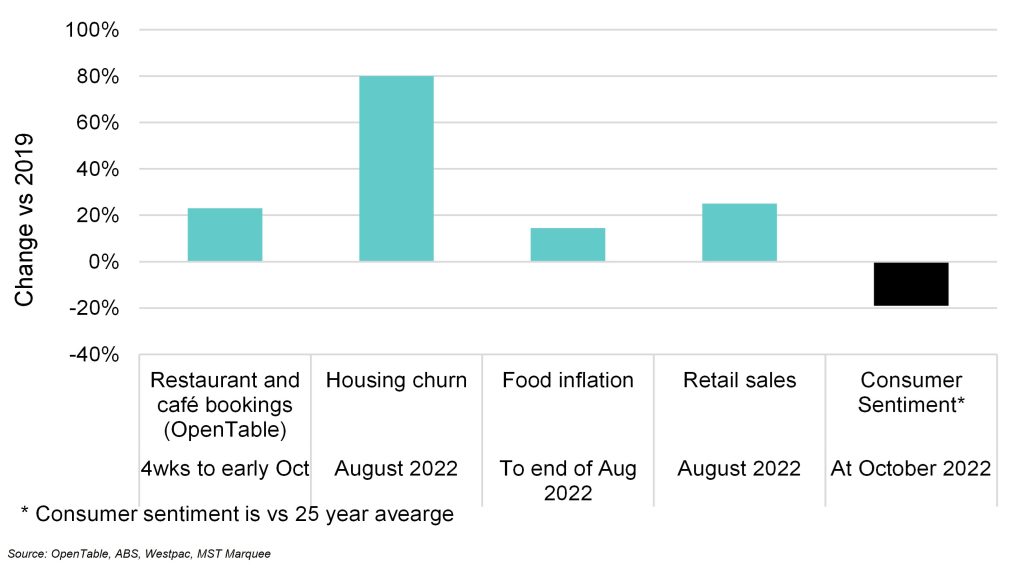

Measuring consumer behaviour vs consumer sentiment

The potential disconnect

12 October 2022

Search result for "" — 691 articles found

Not already a member?

Join now to get all the latest reports in full and stay informed.