Toggle intro on/off

Endeavour (EDV) FY22 result insights

Trade-offs in normalisation path

25 August 2022

Inghams (ING) FY22 result

Tough times to persist a little longer

22 August 2022

Treasury Wine (TWE) FY22 result insights

Gross margin driven growth

22 August 2022

Super Retail (SUL) FY22 result insights

One more half of topline growth

19 August 2022

JB Hi-Fi (JBH) FY22 result insights

The peak is now in sight

17 August 2022

Reporting season preview - Retail, food & beverages for FY22e

The downturn can wait

11 August 2022

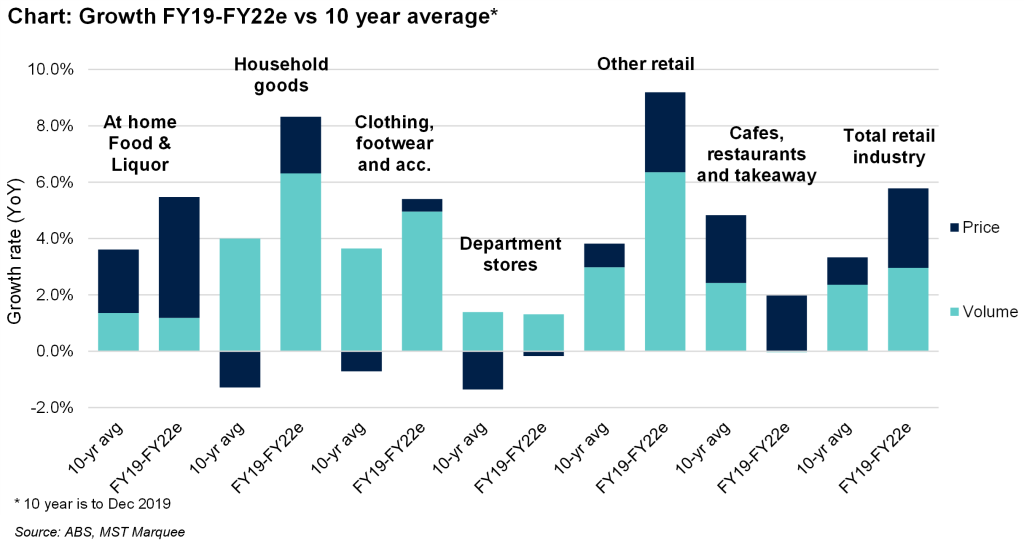

The contribution of price to revenue growth in retail

What mean reverts, price, volume or both?

05 August 2022

Supermarket margins up

Shaping up as a good FY23e

04 August 2022

Retail sales for June 2022

Resilience on display

03 August 2022

Inflation for the June 2022 quarter

Price rises evident and more to come

27 July 2022

Search result for "" — 646 articles found

Not already a member?

Join now to get all the latest reports in full and stay informed.