Toggle intro on/off

Australian inflation for the June 2026 quarter

No “pop” in retail inflation yet

27 July 2026

Presentation: Retail forecasts update April 2025

What happens next?

02 May 2025

Retail forecasts for 2025 - quarterly update

What happens next?

01 May 2025

Price Watch Issue 6 - Retail price drivers

The lead indicators for retail prices

07 July 2023

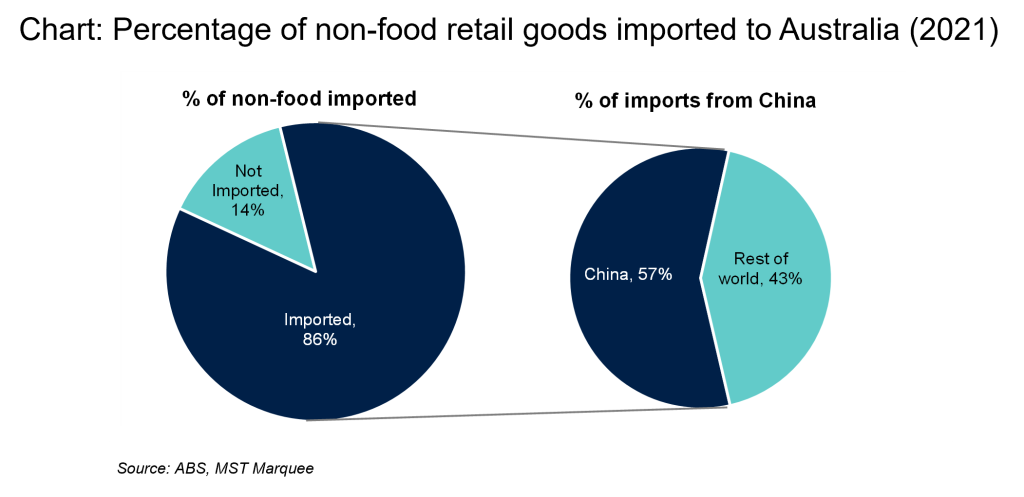

The need to diversify supply chains for Australian retailers

Reliance on China

24 September 2022

Search result for "" — 691 articles found

Not already a member?

Join now to get all the latest reports in full and stay informed.