Toggle intro on/off

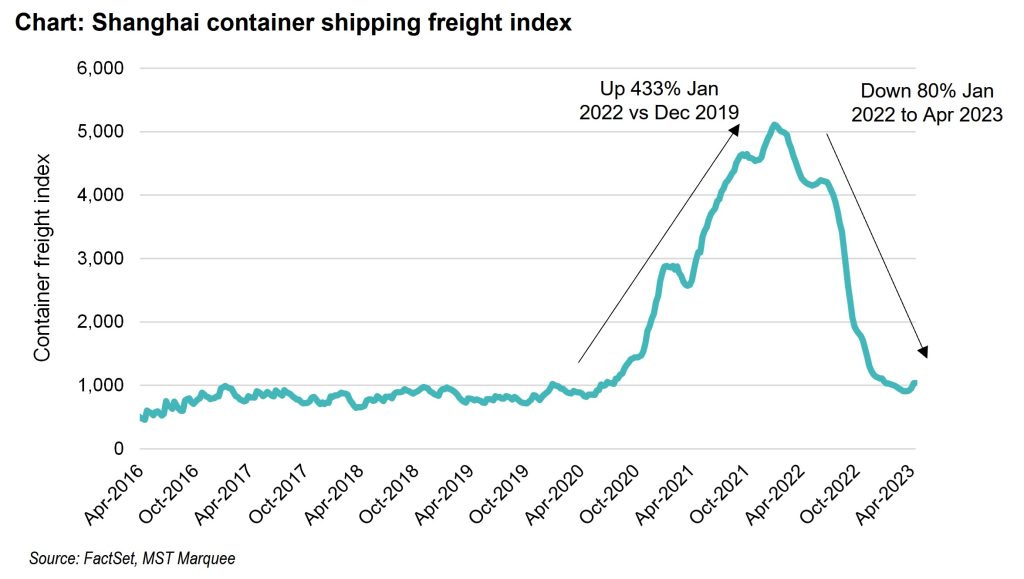

Shipping costs fall back to 2019 levels

The impact on retail inflation

24 April 2023

The Retail Mosaic Issue 6

An inventory balancing act - The short-term pain of excess inventory

07 April 2023

Australian retail sales February 2023

Dispersion rising

05 April 2023

Premier Investments (PMV) 1H23 result insights

Peter Alexander Still Performing

01 April 2023

Price Watch Issue 5 - Price discounts

The tactics and legal limits for retailers

29 March 2023

Treasury Wine (TWE) US 2023 investor tour

Refining the premium wine focus

13 March 2023

Australian retail sales for January 2023

Shift within the retail wallet

07 March 2023

What if retail wages rise 8% in FY24e?

The risk to retailer earnings

06 March 2023

Harvey Norman (HVN) 1H23 result

Earnings normalisation underway

02 March 2023

National accounts for Dec '22 quarter

A new normal emerging

01 March 2023

Search result for "" — 644 articles found

Not already a member?

Join now to get all the latest reports in full and stay informed.